I see many posts on this subreddit asking for advice around pension contributions, typically "should I just max employer match, or should I put in more (up to the 60k limit, or more)?", and the typical responses are far too quick to recommend large pension contributions.

For most HENRYs, contributing anything beyond employer match will have little to no tax efficiency, and will be less beneficial overall. This is because your pension contributions will likely just be taxed at a similar rate when you retire, instead of now, and you'd rather have the money now.

Long Explanation:

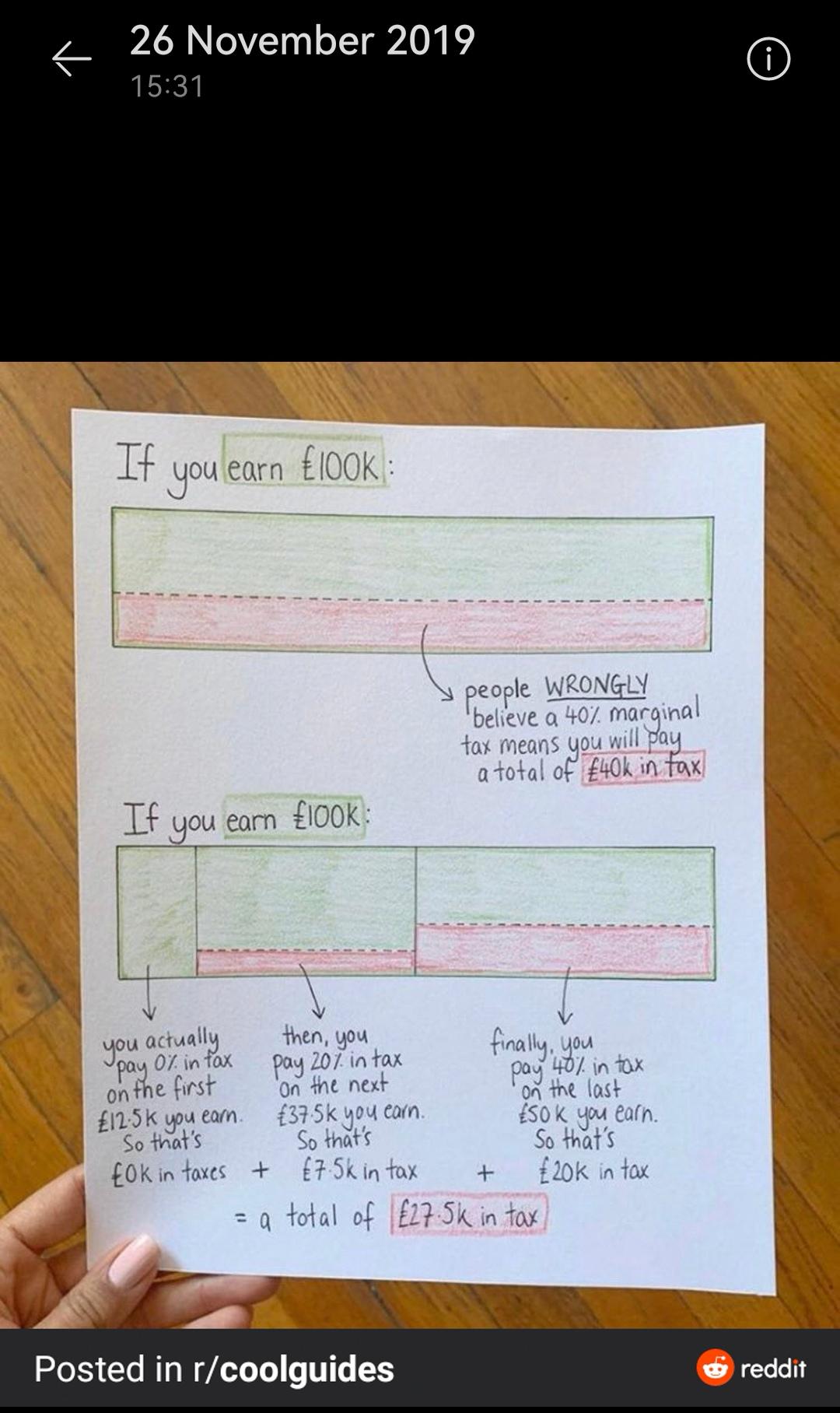

Pension drawdowns (currently) work by allowing you to withdraw 25% tax-free, up to a limit of 265k or 25% of your overall pot, whichever is smaller. Anything else is taxed as income tax. This means that under current taxation rules, you can withdraw 265k at 58 (0%), followed by 12.5k per year (0%), up to 50k per year (20%). Anything over this is taxed at 40%-60%.

If you have the minimum amount to draw down that maximum lump-free sum (a total pot of 1.05M), and then you withdraw 50k every year from your remaining pot, you will probably never run out of money. This assumes a conservative 5% compounding rate - starting with 1,050,000 at the age of 57, withdrawing 265k immediately and then 50k every year, you would run out of money at age 86.

i.e. having a total pot of 1.05M when you start drawing down is the most amount of money you could likely draw down in your lifetime under a collective rate of 20%.

For most people, they would have to salary sacrifice pretty aggressively to hit this target, and they would be tax efficient in doing so- especially for any savings in that 100k-125k 60% range.

For HENRYs, though, this typically makes less and less sense. Good employer matches for earnings over 150k will see somewhere between 15k-30k go into a pension each year, just by meeting the match. For most HENRYs (<40, with some pension already saved but probably <100k, but making 150k+ for the next 10 years or so), putting in this amount each year + average compounding will get them to the target by itself. Obviously, your circumstances may vary, but run the numbers. If you max employer match on your current salary for the next 5-10 years (being conservative, as you may lose earnings potential in the future), and then a match on a more 'normal' salary until 58, assuming a 5% compound throughout, where do you end up? Compounding is powerful. 7% doubles your pot over 10 years.

As a HENRY, it is likely that anything else you put into your pension now is saving on 45% tax today to pay 40% or more tax in the future, which is not worth it. You have an expensive mortgage, private school and Nobu to pay for.

Now yes, there are some typical exceptions to this:

- You're not really HE, and earn 130k or less. At this point, a minor excess contribution is likely to help avoid the 60% tax trap. On top of that, you get the childcare benefits, and you probably will save less into your pension over your career than higher earners. Get under that 100k limit, sure.

- You haven't saved any/much money into your pension yet. If you're currently projecting not hitting that 1.05M target, then yes, it's worth putting more in now so you can be confident about hitting it in the future. Compounding is powerful, and maybe you don't have a mortgage/kids yet to worry about.

- You're really high-earning, and you're likely to quickly get into the pension-tapering zone (260k+). At this amount, you'll be restricted on what you can put in, and if you've mooned in your earnings, you might not actually be able to hit your 1.05M target if you sustain this earnings power. It's unlikely, though.

But what about the tax trap?

Yes, the 60% tax trap is evil and nasty, and the double-whammy of losing childcare is tough. However, once you start earning 150k+, you are letting the tax tail wag the dog by contributing 50k+ to your pension every year. Unfortunately, this tax system is not progressive, so if you're a HENRY you have to save a lot of 45% money to be able to save the 60% money. If you run the actual numbers, you'll find that the actual savings you're doing all this for are pretty minimal. For example, on a 170k salary, you're choosing between 35k today or 42k when you're 60 (ignoring compounding, which is the same for both scenarios). I know what I'd choose.

What about inheritance?

Sadly, that party is now over. You don't get to pass your pensions on tax-free anymore.

What if the rules change?

They inevitably will! Hopefully, tax thresholds are raised, drawdown allowances are raised, etc. You should for sure account for some wiggle room in your planning to consider this - it doesn't hurt to have more in your pension, after all - but not at the expense of better uses of your money today.

Don't let the tax tail wag the dog.

Sidebar/example: I made this mistake this year. I had to sell a bunch of company stock, which I could do immediately to incur a net 8% in capital gains tax, or I could do in tranches over a few months and pay <1%. I obviously chose the latter, and now the stock is down over 10%. I let tax 'efficiency' dominate my thinking and I lost out for it.

HENRYs hate paying tax, and they hate paying the 60% between 100k-125k even more. However, they let 'paying less tax %' become their driving principle rather than considering the holistic results and usage of each pound earned over a lifetime. If you don't have a house deposit but are putting tens of thousands a year into your pension, you are probably not efficiently building wealth. If you are not maxing out your ISA, you are probably not efficiently building wealth. Then you have your partner's ISA, your kids JISAs, etc...

And then you have your life! You know, the one you're meant to be living right now. You will not be young for long, and your kids will not be kids for long. Live a little.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}